The Russian Ruble has slumped harder against the US Dollar as it trades at a near 17-month low.

President Vladimir Putin’s economic advisor blames loose monetary policy for the rapid depreciation of the Ruble.

The Bank of Russia blames the country’s shrinking trade balance as its current account surplus fell 85% YoY from January to July.

Russian Ruble fell to 17-month record levels of 100 per USD on Monday as the country battles a shrinking trade balance. The current account surplus dropped by 85% YoY from January to July as Western sanctions pushed the country further.

Russian Ruble trades at 100 against the US dollar

Since Russia invaded Ukraine, the country has been experiencing turmoil with holding up the value of the Rubble as harsh economic sanctions from the West have been imposed on it. The West has also been aiding Ukraine economically in the war, which prompts Russia to spend more to sustain its offensive missions.

As an aftermath, the Russian Ruble slid past the 100 mark against the USD on Monday, nearing a 17-month low. The country’s presidential economic advisor blamed loose economic and monetary policy for weakening the Rubble.

This year alone, the Ruble has lost value by 30% against the greenback. This situation has prompted the Bank of Russia to blame the country’s balance of trade as its current account surplus fell 85% year-on-year from January to July.

“A weak ruble complicates the restructuring of the economy and negatively affects the population’s real incomes. In the interests of the Russian economy — a strong ruble,” President Putin’s economic advisor Maxim Oreshkin said.

Last week, the Bank of Russia halted foreign currency purchases for the remainder of the year to shore up the currency as the country battles increasing isolation from Western sanctions.

While fears of rising inflation grip Russia, its GDP exceeded expectations and grew by 4.9% year on year in Q2, per figures from the Federal State Statistics Service, which s a rebound from a 1.8% contraction in Q1. Keep watching Fintech Express for more updates on finance and other fintech-related developments.

PayPal is set to launch a cryptocurrencies hub for select users

The adoption of crypto solutions is part of the platform’s plan to reinvent itself as a crypto-inclusive platform

PayPal recently launched a stablecoin in a push to rebrand as a crypto-inclusive payments platform. On Monday, it also announced it was also rolling out a cryptocurrency hub for select users.

Paypal’s crypto endeavors continue

Paypal’s new cryptocurrencies hub will allow for the sale and purchase of crypto assets, among other crypto-friendly functionalities. The payment company’s recent terms and conditions update detail the prerequisites for crypto users interested in trying out the new platform.

The Cryptocurrencies Hub service will also facilitate the payment of purchases via PayPal using money stored after the sale of crypto assets. It will also be crucial in the conversion between PYUSD and other crypto assets.

PayPal further released a statement explaining that any balances in the Cryptocurrencies Hub represent a user’s ownership of the amount of each crypto asset displayed. As such, users will not hold the digital crypto assets in their crypto asset balance.

Since this feature is still in the pilot phase, not all PayPal users will get to explore it. The eligible users of the Cryptocurrencies HIb must have “a personal PayPal account and a Balance Account in good standing.” Additionally, PayPal will verify the required identifying information like names, taxpayer identification numbers, and physical addresses.

“You can only use your Cryptocurrencies Hub as part of your Balance Account by accessing it through your personal PayPal account. If you are a Hawaii resident, we will not allow you to establish a Cryptocurrencies Hub now.”

Upon launch, the Cryptocurrencies Hub will be connected with PayPal users can access it using existing credentials. These developments come days after the company launched a highly divisive crypto stablecoin pegged on the US Dollar, the PYUSD.

Some feel that it may propel the mainstream adoption of crypto assets, while others believe it may bring trouble in decentralization as the company has its smart contracts infused with functions like “freeze funds” and “wipefrozenfunds” which goes against the spirit of decentralization.

Keep watching Fintech Express for more updates on this and other fintech-related developments.

The UK economy has defied all odds and posted an impressive 0.2% growth despite projections that it would contract in Q2.

The growth came as household expenditure rose in tandem with manufacturing output.

Economists still fear the effects of high-interest rates are not fed through, and pain is yet to be lifted from British markets.

UK economy has seen a surprise 0.2% growth in Q2 as manufacturing output and household expenditure rose though the effects of high-interest rates are still shaking the markets.

UK posts a Q2 2023 surprise growth

The UK has been on the verge of a reversed economic growth this year following its January 2020 Brexit and the post covid 19 economic challenges. The country has been battling high inflation rates of up to 12%, which has necessitated the introduction of tighter banking measures.

The BoE has hiked interest rates making borrowing more expensive for nationals and investors in Britain. While the interest rates are working to bring down the inflation levels, the economy has been hit by pain in its markets. More and more households cannot afford to pay their mortgages, while businesses have been cutting their expenditures.

These economic outlooks were expected to drag the UK economy into contraction in Q2, only to bounce back with an impressive 0.2%. The jump is due to increased manufacturing output and spending rates.

The economy expanded by 0.5% in June, beating a forecast of 0.2% and monthly GDP growth of 0.1% in May and 0.2% in April. Manufacturing output grew by an impressive 1.6%, production followed by 0.7%, and services posted a fair 0.1% growth.

On Friday, the Office for National Statistics report said that the strong growth in household and government consumption in terms of expenditure faced price pressure over three months though it was moderated in the previous quarter.

Recession bloodbath fears still looming

Though the UK economy still has ‘legs, ’ the effects of high-interest rates are not necessarily over. BoE hiked rates by 25 basis points in August to 5.25%, and inflation is still running wild, meaning further hikes will be necessary. The UK inflation rates are the highest, around 7.9%, which means the government will not meet its 2% target for the year till Q4 2024.

As such, policymakers will observe the market ahead of the September rate hike decision meeting. Ruth Gregory, deputy chief U.K. economist at Capital Economics, said in a Friday note that the consultancy still forecasts a mild recession for the country later in the year as the impact of higher interest rates is felt.

Keep watching Fintech Express for updates on this and other fintech-related developments.

Asset tokenization is one of the most promising and disruptive blockchain-related technological innovations. This revolutionary concept has the potential to reshape the way we view, trade, and manage traditional assets, offering increased accessibility, liquidity, and efficiency. In this article, we delve into the concept of asset tokenization and explore how it is leading the way toward the future of asset management.

I. Understanding Asset Tokenization

Asset tokenization is the process of converting ownership rights to a real-world asset into digital tokens on a blockchain. These tokens represent ownership or fractional ownership in the underlying asset, which can range from real estate properties and works of art to commodities and even income streams from revenue-generating assets. Asset tokenization aims to digitize and democratize ownership, enabling a wider range of investors to access and invest in previously illiquid or difficult-to-divide assets.

II. The Mechanism of Asset Tokenization

Asset tokenization involves several key steps that transform a physical asset into digital tokens:

Asset Identification and Evaluation: The first step involves identifying the asset to be tokenized and conducting a thorough evaluation to determine its value, legal status, and potential for fractional ownership.

Legal Structuring: Legal experts design the token structure, defining ownership rights, responsibilities, and potential revenue distributions. This step ensures that the tokenized asset adheres to relevant regulations.

Smart Contract Development: Smart contracts, self-executing code on a blockchain, are created to automate the issuance, trading, and management of asset tokens. These contracts outline token transfer rules, ownership changes, and other interactions.

Token Creation: Digital tokens are generated on a blockchain platform, each representing a specific fraction or unit of ownership in the underlying asset. These tokens are typically categorized as security or utility tokens, depending on the asset and its regulatory implications.

Token Offering: The asset tokens can be offered to a wide range of investors through Initial Coin Offerings (ICOs), Security Token Offerings (STOs), or other regulatory-compliant fundraising methods.

Secondary Market Trading: Once issued, asset tokens can be traded on secondary markets, enabling investors to buy and sell fractional ownership in the asset. This liquidity enhances accessibility and eliminates the barriers associated with traditional illiquid assets.

III. Advantages of Asset Tokenization

1. Enhanced Liquidity: Asset tokenization unlocks liquidity for traditionally illiquid assets, such as real estate and art. Investors can trade fractions of an asset on secondary markets, promoting efficient price discovery and reducing holding periods.

2. Accessibility: Tokenization democratizes access to investment opportunities by allowing smaller investors to participate in asset ownership. Fractional ownership makes high-value assets accessible to a broader audience.

3. Transparency and Security: Transactions and ownership records are recorded on an immutable blockchain, providing transparency and reducing the risk of fraud. This transparency also streamlines auditing and compliance processes.

4. Reduced Intermediaries: Traditional asset transfers involve multiple intermediaries, leading to higher costs and longer settlement times. Asset tokenization eliminates or reduces the need for intermediaries, lowering costs and increasing efficiency.

5. Global Market Reach: Tokenization facilitates cross-border investment by enabling seamless transactions and eliminating currency conversion challenges.

IV. Transforming Asset Management

1. Diversification: Asset tokenization empowers investors to create diversified portfolios with exposure to various asset classes, reducing risk and enhancing potential returns.

2. Automation and Efficiency: Smart contracts automate various aspects of asset management, such as dividend distributions and compliance with regulatory requirements, reducing administrative burdens.

3. Real-time Valuation: Digital tokens enable real-time valuation of assets, providing investors with accurate and up-to-date information about their portfolio’s performance.

4. Fractional Ownership: Fractional ownership allows investors to tailor their investment amounts to their preferences and financial capabilities, enabling more people to participate in lucrative opportunities.

5. Reinventing Finance: Asset tokenization challenges traditional financial structures and introduces new ways of raising capital, democratizing investments, and promoting financial inclusion.

V. Challenges and Considerations

While asset tokenization holds immense potential, it also comes with challenges:

1. Regulatory Compliance: Asset tokenization must navigate complex regulatory landscapes, with different jurisdictions having varying rules for security tokens and utility tokens.

2. Technical Infrastructure: Developing secure and efficient smart contracts and blockchain infrastructure requires technical expertise.

3. Investor Education: Educating investors about asset tokenization’s benefits, risks, and mechanics is crucial for widespread adoption.

4. Market Adoption: Widespread adoption depends on acceptance by traditional financial institutions, regulatory bodies, and investors.

VI. Conclusion

Asset tokenization is reshaping the landscape of asset management, bringing together the worlds of traditional finance and emerging blockchain technology. By converting ownership rights into digital tokens, asset tokenization enhances liquidity, accessibility, and efficiency while transforming the way assets are managed and invested.

As the technology matures and regulatory frameworks evolve, asset tokenization has the potential to unlock new investment opportunities, democratize finance, and pave the way for a more inclusive and dynamic future of asset management.

Cryptos have reshaped the financial landscape, introducing innovative concepts and challenging traditional economic paradigms. One such concept is classifications into two distinct categories: inflationary and deflationary cryptocurrencies.

These terms are derived from the broader economic concepts of inflation and deflation, and they have important implications for the value, usage, and adoption of different cryptocurrencies. In this article, we delve into inflationary and deflationary cryptocurrencies, exploring their characteristics, benefits, drawbacks, and potential impact on the global economy.

Inflation and Deflation: A Brief Overview

Before delving into the specifics of inflationary and deflationary cryptocurrencies, it’s crucial to understand the underlying economic concepts.

Inflation occurs when the general price level of goods and services in an economy rises over time. This phenomenon erodes the purchasing power of money, as each currency unit buys fewer goods and services. Central banks often use controlled inflation as a tool to stimulate economic activity, encourage spending, and manage debt.

Deflation, on the other hand, refers to a decrease in the general price level of goods and services. While it might seem beneficial, sustained deflation can lead to reduced consumer spending, business contraction, and economic stagnation. Central banks typically seek to avoid deflation by implementing monetary policies to promote stability and growth.

Inflationary Cryptocurrencies: Features and Implications

Inflationary cryptocurrencies are digital assets designed to have a controlled and predictable increase in their supply over time. This mimics the concept of controlled inflation in traditional economies and contrasts with the fixed supply of assets like Bitcoin.

Characteristics of Inflationary Cryptocurrencies:

Controlled Supply: Inflationary cryptocurrencies are often governed by algorithms that determine the rate of new token issuance. This controlled supply mechanism aims to balance stability and incentivizing network participation.

Stimulating Activity: Proponents of inflationary cryptocurrencies argue that a controlled increase in supply encourages spending, investing, and network utilization. It incentivizes users to transact and use the cryptocurrency for various purposes, fostering a dynamic ecosystem.

Reduced Scarcity: Inflationary cryptocurrencies may lack the scarcity-driven value proposition of deflationary assets like Bitcoin. However, this can make them more suitable for everyday transactions, as people are less likely to hoard them for speculative purposes.

Implications of Inflationary Cryptocurrencies:

Stable Pricing: Inflationary cryptocurrencies may experience more stable pricing than highly volatile deflationary counterparts. This stability can make them more attractive for merchants and consumers seeking a reliable exchange.

Economic Stimulus: Just as controlled inflation can stimulate economic activity in traditional economies, inflationary cryptocurrencies may help drive adoption and encourage spending within their respective ecosystems.

Potential Drawbacks: Critics argue that inflationary mechanisms could lead to long-term devaluation, reducing the overall purchasing power of the cryptocurrency. The challenge lies in finding the right balance of inflation to avoid both hyperinflation and economic stagnation.

Deflationary Cryptocurrencies: Features and Implications

Deflationary cryptocurrencies are characterized by a fixed or decreasing supply over time, potentially increasing their value as demand rises and supply remains constant or reduces.

Characteristics of Deflationary Cryptocurrencies:

Limited Supply: Deflationary cryptocurrencies are often designed with a capped supply, such as the case of Bitcoin, which has a maximum supply of 21 million coins. This limited supply is intended to mimic precious resources like gold.

Scarce and Valuable: The scarcity-driven nature of deflationary cryptocurrencies can lead to increased perceived value over time. This characteristic attracts investors and individuals looking to preserve their wealth.

Digital Gold: Deflationary cryptocurrencies are sometimes referred to as “digital gold” due to their potential to serve as a store of value and hedge against traditional economic uncertainties.

Implications of Deflationary Cryptocurrencies:

Hedging Against Inflation: Deflationary cryptocurrencies can serve as a hedge against traditional fiat currencies that are susceptible to inflationary pressures. Investors may flock to these assets during periods of economic uncertainty.

Hoarding and Reduced Spending: The potential for future value appreciation might lead to hoarding and reduced spending, which could hinder their use as a medium of exchange for everyday transactions.

Economic Challenges: A deflationary cryptocurrency’s fixed supply could lead to economic challenges in the long term, including reduced liquidity and potential economic stagnation due to decreased spending.

Balancing Act: Finding the Optimal Approach

The debate between inflationary and deflationary models is ongoing in the realm of cryptocurrencies. Both approaches have merits and drawbacks, and the optimal solution likely lies in a nuanced combination of these models.

Hybrid Models: Some projects are exploring hybrid models that combine elements of both inflation and deflation. These models attempt to balance stability, adoption, and scarcity-driven value appreciation.

Economic Experimentation: Cryptocurrencies provide a unique opportunity for economic experimentation, allowing developers and communities to test different monetary policies in a digital environment.

Consideration of Use Case: The suitability of an inflationary or deflationary model depends on the specific use case of the cryptocurrency. For instance, a cryptocurrency facilitating everyday transactions might benefit from controlled inflation, while a store of value might lean towards a deflationary model.

Conclusion

Inflationary and deflationary cryptocurrencies represent two divergent approaches to the fundamental economic challenge of maintaining price stability and encouraging economic activity. Each model has its implications for adoption, use, and value appreciation. As the cryptocurrency landscape evolves, new models and approaches will likely emerge, further enriching the diversity of digital assets available to users and investors.

It’s important to recognize that cryptocurrency is still relatively young, and the long-term effects of different supply models are yet to be fully understood. As the industry matures and more data becomes available, a clearer picture will emerge regarding the impact of inflationary and deflationary mechanisms on the broader economy and financial ecosystem. In the meantime, investors, developers, and users should remain vigilant and informed as they navigate the exciting world of cryptocurrencies and their underlying economic principles.

Financial responsibility forms the bedrock of a secure and prosperous life. In today’s dynamic and fast-paced world, understanding and practicing financial responsibility are essential skills that contribute to a stable financial future. This article serves as a comprehensive guide to the fundamentals of financial responsibility, providing readers with verified and unbiased information that empowers them to make informed decisions. We will delve into key concepts, strategies, and practical tips that individuals can incorporate into their lives to achieve financial well-being.

I. Defining Financial Responsibility:

Financial responsibility refers to the diligent management of one’s financial resources, encompassing various aspects such as budgeting, saving, investing, and debt management. It involves making informed choices that align with one’s financial goals and values, while also accounting for unexpected expenses and long-term aspirations.

II. Budgeting: The Foundation of Financial Responsibility

Creating a Budget: A budget is a crucial tool that allows individuals to track and control their income and expenses. Start by calculating total monthly income, including salary, freelance earnings, and other sources. Then, categorize expenses into fixed (rent, utilities, insurance) and variable (entertainment, dining out). Allocate funds for each category and ensure that expenses do not exceed income.

Tracking Expenses: Regularly monitor and record expenses to identify spending patterns. Utilize apps and software to streamline the process and gain insights into areas where adjustments can be made.

III. Saving and Investing: Building a Secure Future

Emergency Fund: Establish an emergency fund equivalent to three to six months’ worth of living expenses. This fund acts as a safety net during unforeseen events like medical emergencies or job loss.

Investment Strategies: Diversify investments across different asset classes such as stocks, bonds, and real estate. Conduct thorough research or consult with financial professionals to make informed investment decisions aligned with risk tolerance and financial goals.

IV. Debt Management: Navigating Borrowing Wisely

Understanding Debt: Not all debt is equal. Differentiate between “good” debt (education, home mortgage) and “bad” debt (high-interest credit card debt). Prioritize paying off high-interest debts to reduce financial strain.

Responsible Borrowing: When taking on new debt, ensure that the monthly payments fit within the budget. Compare interest rates, terms, and fees before committing to a loan.

V. Long-Term Financial Planning: Achieving Milestones

Retirement Planning: Start saving for retirement early through retirement accounts like 401(k)s or IRAs. Take advantage of employer-matching contributions and explore investment options for long-term growth.

Education Planning: If applicable, consider setting up education savings accounts (e.g., 529 plans) to prepare for the cost of higher education for yourself, children, or dependents.

VI. Lifestyle and Financial Responsibility:

Differentiating Wants from Needs: Practice conscious spending by distinguishing between essential needs and discretionary wants. Avoid impulse purchases and consider the long-term impact on financial goals.

Living Below Means: Strive to live below your means to allocate resources toward savings and investments. Avoid lifestyle inflation that can hinder financial progress.

Conclusion:

Incorporating the basics of financial responsibility into your life is a transformative journey that lays the foundation for financial security and success. By mastering budgeting, saving, investing, and debt management, you empower yourself to make sound financial decisions and achieve both short-term goals and long-term aspirations.

Remember, financial responsibility is an ongoing commitment that requires continuous learning and adaptation to changing circumstances. Embrace these principles, and you’ll embark on a brighter financial future. Keep watching Fintech Express for similar content updates.

(Note: This article aims to provide general information about financial responsibility. Readers are encouraged to consult with qualified financial advisors before making any financial decisions.)

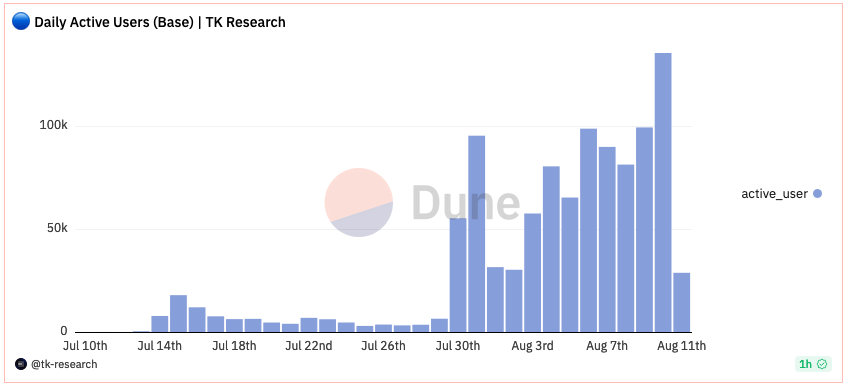

Coinbase layer 2 network Base set a new record yet after hitting 136,000 daily users on AUG 10

On the same day, about 30% of the users were new.

Coinbase layer 2 network Base has registered an impressive 136K users in a day despite the exchange being under US SEC investigations and legal battles.

Coinbase layer 2 network Base gaining traction despite legal troubles

On-chain analytics show that over 136K users accessed the Coinbase layer 2 network Base on August 10, just a day after its launch, a record performance for a new blockchain.

Nearly 42,000 users accessed the network for the first time on August 10 though its record high for new users was on July 31 when it hit the registered 60,000 mark. Data from Cryptorank.io show that the blockchain stood as the 4th largest in daily transactions among layer 2 networks, just behind zkSync Era, Arbitrum, and Optimism.

Base Now Ranks 4th in Daily TPS Among Layer 2 Solutions 🔵#Base Layer 2 launched its mainnet yesterday and is showing robust growth in active users and transactions. Now it ranks 4th by daily TPS (Transaction per second). pic.twitter.com/pnYF0tk7b0

The network launched on August 9 officially and has been pulling numbers despite the exchange being in a legal battle with the US SEC. It is being charged for acting as a securities broker despite not having had the chance to register ‘fully’ with the regulator regarding the complainants in the past.

However, the case is still far from being determined. Keep watching Fintech Express for details and updates as soon as they happen.

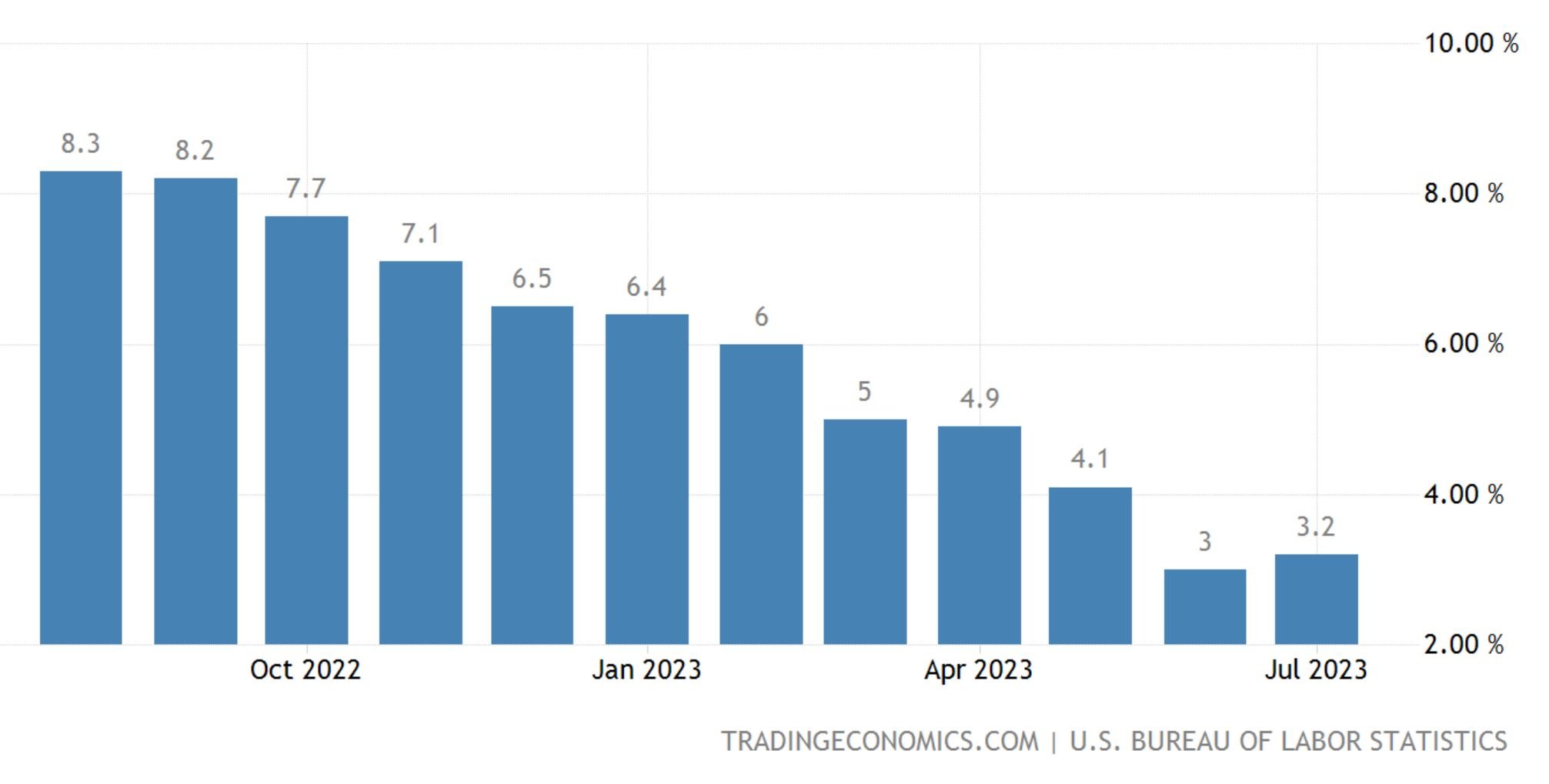

July US CPI inflation has come slightly higher than in June but still sending hope across international markets.

July had a lower CPI inflation of 3.2% following the introduction of another interest rate hike to help fight inflation.

Analysts believe Interest rates should be maintained around 5% despite falling inflation.

Following the announcement of lower-than-expected US CPI in July (3.2%), international markets have started rising (both stock and cryptos). However, analysts still feel that interest rates should hold up at the current levels to keep inflation in check.

US CPI sends a wave of hope across global markets

Data from the Bureau of Labor Statistics indicate that the annual US CPI spiked to 3.2% in July, lower than the expected 3.3%. As a result, the crypto and Stock markets have begun rising.

Bitcoin Price has started rising from the 29,457 mark hit at 11:50 E.A.T to the 29,568 mark at the time of writing following the bulling CPI data. At the same time, the STOXX 600 index has risen from 462.35 points to 462.85 points at the time of writing following the news.

The overall US CPI has moved up to 3.2% from June’s 3% ending a streak of 12 consecutive declined YoY but still sending hope across international markets.

The US Core CPI (removing food and energy) came in at 4.7%, a drop YoY (Year-over-Year), the lowest level since October 2021. At the same time, some sectors topped in inflation numbers as follows:

Food away from home inflation: 7.1%

Shelter inflation: 7.7%

Transport inflation: 9%

At the same time, analysts now believe that the US should not deem the fight against inflation as done. A further interest rate hike was done in July, yet the inflation rates did not drop significantly from June. As such, it would be best to hold up the current rates for a little longer.

Federal Reserve Chair Jerome Powell said in a June meeting that they expect two interest rate hikes this year to keep the fight against inflation alive. This decision is expected to bear one more interest rate hike between August and December this year as the central bank targets inflation of just 2% by the end of the year. July’s US CPI spike now adds more possibility of rates hike in August or September to calm the markets down.

Keep watching Fintech Express for more updates on finance and other fintech related developments.

France has updated its crypto licensing rules to match MiCa legislation

The new amendments will come into effect on January 1, 2024, around the same time as the MiCA legislation

Applicants for DASP regulatory licenses in France starting in the year 2024 will have to follow MiCA legislation as the country has updated its licensing regime. The Eurozone is expected to enforce MiCA regulation in 2024, ushering in a new era of regulated blockchain and crypto adoption.

France ramps up crypto licensing rules to match MiCA

A press release from Autorité des Marchés Financiers (AMF), France’s main financial authority ushers in new policies that will see digital asset service providers take an “enhanced” registration process to comply with crypto licensing rules to match MiCA legislation.

The new registration requirements are captured by the AUMF’s article 721-1-2 of the MAF General Regulation that will include systems for managing conflict of interests, more disclosure obligations, and prohibition to use client assets without their consent, among others.

While these regulations were set in on January 1, 2024, any crypto exchange licensed before the new amendments will benefit from much lighter requirements set, which is protected by a “Grandfather clause” that comes as a simpler version of the MiCA regulatory framework.

Keep watching Fintech Express for more updates on this and other fintech-related developments.

Microsoft has announced a partnership with Aptos labs for AI solutions, driving Aptos tokens’ prices high.

Microsoft has been pushing its limits to stay competitive amid the rise of AI among tech companies like Meta and OpenAI.

Aptos Labs, started by former Facebook employees, has partnered with Microsoft to develop AI solutions. Within minutes of announcing the deal, the Aptos token surged about 15% to around $7.70.

Aptos Labs to be Microsoft’s partner in new AI adventure

In this arrangement, Aptos Labs will leverage Microsofts infrastructure to deploy new AI solutions encompassing blockchain technology. One of the solutions that Aptos Labs is eyeing is an AI chatbot called Aptos Assistant, which will be able to answer any question regarding the Aptos ecosystem and provide resources for developers who want to build on the network.

In the press release, Aptos Labs indicated that it was also integrating Move, its native programming language, onto GitHub’s copilot service. This AI programming tool will support developers in their building efforts.

Regarding the arrangement, Microsoft’s General Manager of AI and emerging technologies said they aim to democratize blockchain technology to enable users to board onto Web 3 seamlessly.

“By fusing Aptos Labs’ technology with the Microsoft Azure Open AI Service capabilities, we aim to democratize the use of blockchain enabling users to seamlessly onboard to Web3 and innovators to develop new exciting decentralized applications using AI.”

Microsoft has been pushing its limits in developing AI tools, mostly via partnerships with other companies. It recently struck a partnership deal with OpenAI to incorporate the widely known ChatGPT AI Bot into its search engine, Bing. The deal was done to keep the company in touch with emerging companies before it releases its AI products.

Now, it has struck a deal with Aptos Labs to push its presence in both the AI and blockchain industries, hoping that it would help to onboard even more users to emerging technologies as the hype for both blockchain and AI industries keep growing.

Keep watching Fintech Express for more updates on this and other fintech-related developments.