The Decentralized Finance sector is performing well amid regulatory uncertainties.

DeFi tokens have shown some of the highest gains among other cryptos as regulators increase their oversight.

Decentralized Finance (DeFi) tokens have posted strong gains amid increased regulatory oversight in the past 28 days. This trend shows that people turn to decentralized finance as a hedge against centralized oversight.

DeFi tokens performs well amid regulatory uncertainties

DeFi tokens have posted strong price gains over the past month as the crypto industry battles a hungrier regulatory whip. Regulators worldwide, including but not limited to UK FCA and the US SEC, have gone after crypto strongly in June and part of July, sending shivers down investors’ spines.

However, it seems the industry has found an alternative in the Decentralized Finance sector. The decentralized finance sector is where no one controls the governance of a protocol; thus, the governments find it hard to exert their power on the industry. As such, it is not usually affected by harsh regulations, and it benefits as investors take it as a hedge against tough regulatory oversight.

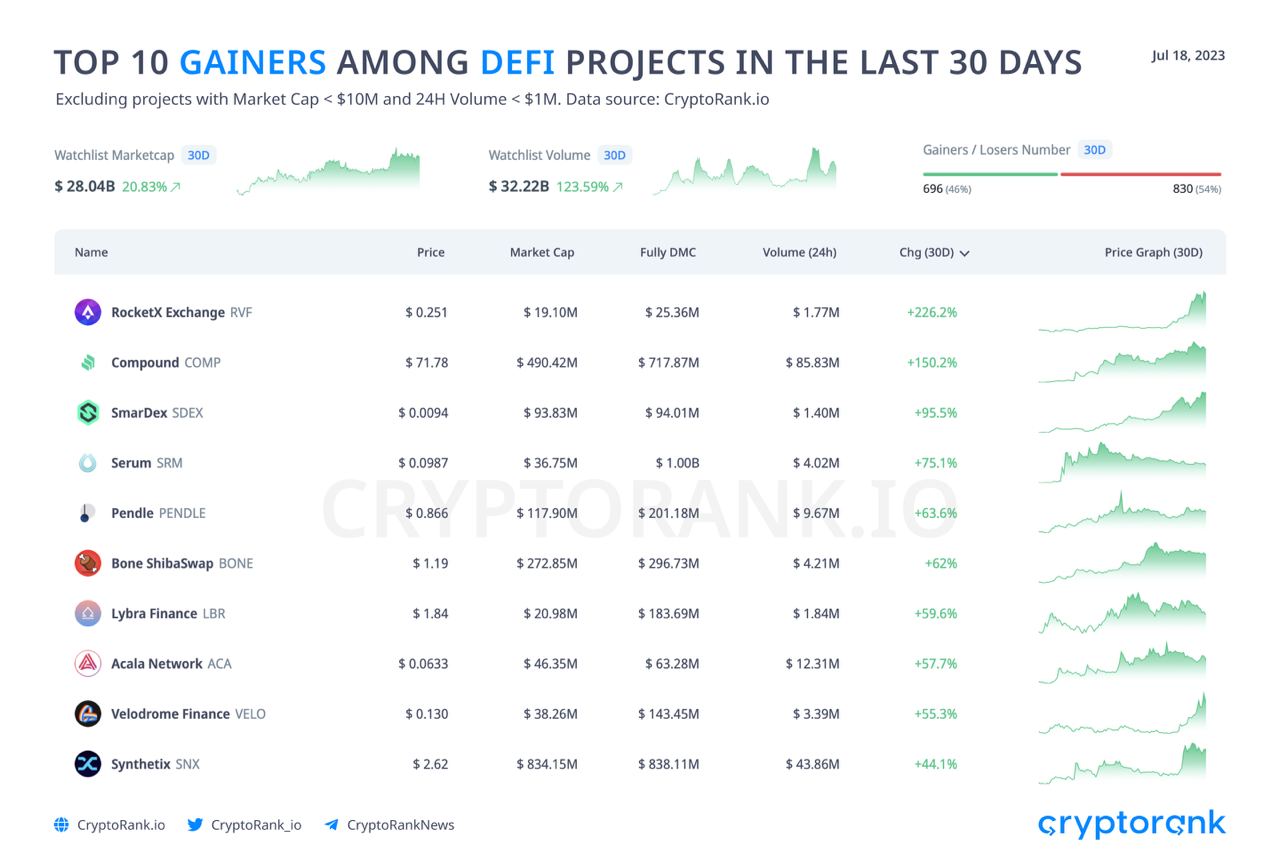

Over the past month, DeFi projects have shown one of the highest gains among other categories. RocketX Exchange +226.2%, Compound +150.2%, and SmarDex +95.5% are the most significant gainers over the past 30 days. At the same time, the category’s market cap and trading volume increased by 20.8% and 123%, respectively.

Keep watching Fintech Express for more updates on DeFi and other fintech-related

The US SEC has accepted Valkyries BRRR spot Bitcoin ETF for review

The development comes soon after the regulator accepted Blackrock’s spot bitcoin ETF application for review as well

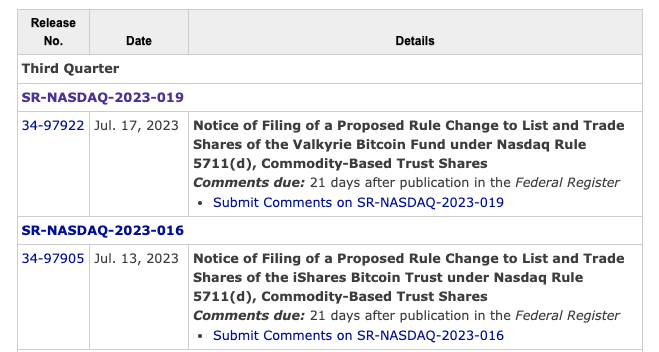

Valkyries BRRR spot Bitcoin ETF is now officially under the US SEC review process after the regulator expressed that it had been satisfied with the filing. This ETF was named ‘BRRR’ after a popular meme in the Bitcoin community that refers to the money printer sound.

Valkyries BRRR spot Bitcoin ETF accepted for review by the SEC.

The US SEC has begun reviewing the popular Valkyries BRRR spot bitcoin ETF. This ETF, named after a popular meme in the crypto industry, was filed as an answer to BlackRock’s spot Bitcoin ETF.

BlackRock’s CEO Larry Fink has moved from thinking that Bitcoin is a scam in 2017s to acknowledging that it’s a ‘digital gold’ and wanting to expose his investors to it. Other TradFi institutions have joined the queue to file for similar assets, including Valkyrie.

Per data from the SEC’s Nasdaq rulemaking list, Valkyries BRRR spot Bitcoin ETF proposal has entered an official docket as of July 17. This filing was accepted after BlackRock’s was accepted four days apart on July 13.

This acceptance opens the road for US SEC officials to look into the key details of the filing and determine if it is fit to be offered to US markets. These ‘TradFi crypto take over’ filings are expected to be approved, opening flood doors of institutional investors to the crypto market.

However, only time will tell what happens now that the US SEC is not the biggest fan of how the crypto industry is being run. Keep watching Fintech Express for more updates on this and other fintech-related developments.

The crypto community has expressed disdain over poor management and centralization in the Multichain crypto ecosystem.

Multichain experienced a series of ‘hacks,’ which have all been confirmed to be inside jobs, resulting in a series of companies being forced to close down.

Multichain Bridge ‘hack’ has sent a ripple of distrust in the crypto industry after what investors thought was a hack was revealed to be an inside job. Multichain is forced to close down as it does not have operational funds to continue operating since all control was under an arrested CEO, and all validators have been kicked out of the MPC node servers.

Multichain Bridge mismanagement stirs the pot

The crypto community is not buying into the Multichain hacking and CEO disappearance story, as the industry is counting losses from the misfortune. According to the company, Multichain Bridge CEO Zhao Jun was arrested in May 2023.

Since his disappearance, Multichain Bridge has been left with crippled systems. Its MPC node validators were kicked out of the servers, and no one else had access to them or Jun’s cloud server, or so it was thought. This state of operation was the case until it was discovered that Jun’s sister was transferring investor funds from MPC accounts to a personal EOA address.

She was also arrested by the same Chinese authorities that reportedly took Zhaojun. Now, Multichain has to wind down its operations. This misfortune has sent a wave of distrust and disdain across the crypto space. Multichain was one of the largest bridges and had thousands of users.

Talking to Fintech Express, DeFi solutions provider Bracket Labs called on DeFi projects to recheck their decentralization approaches and avoid falling for a similar centralization of power as seen in the Multichain saga.

“It is extremely disappointing to hear that the disappearance of the Multichain founder could lead to a shutdown of the protocol because of centralized back-end infrastructure. Even though the MPC nodes themselves are running properly, the fact that they are node servers running on the founder’s personal cloud server account is concerning.

This is a wakeup call for all DeFi projects to verify that they do not rely on any single individual or infrastructure provider/vendor,” Bracket Labs said.

Aftershock events of the Multichain Bridge meltdown

As a result of poor management in the ranks of Multichain Bridge, multiple investors have been affected. Some projects will even be forced to close down. Such a project is Geist Finance. Geist Finance is a lending protocol that held its assets on Multichain. However, it has no choice but to wind up its operations permanently following the misfortune.

1/4 Geist Finance on Fantom REKT due to Multichain bridge fiasco.

A fork of Aave, Geist is a lending/borrowing protocol that uses Chainlink oracle.

Yet, the Chainlink tracks prices of real native tokens, while they were trading at around 0.22 to the dollar on Fantom. pic.twitter.com/Ja1whaHX7n

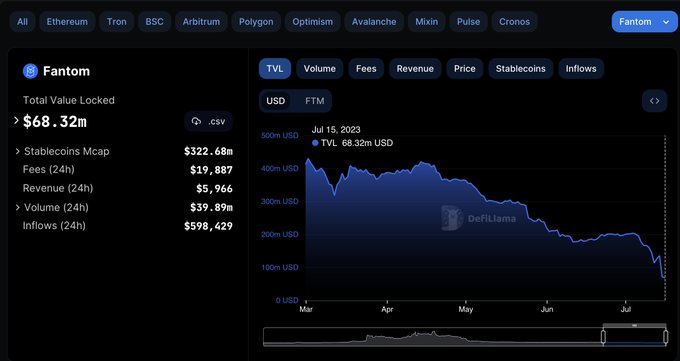

The Ripple effect has also hurt the Fantom network, as the blockchain harbored Multichain. Multichain was its largest bridge, meanings its shutdown resulted in lower network usage. In a July 17 update, Fantom expressed that it was disappointed to hear about Multichain but had found a solution.

“We are deeply disappointed to hear about the latest Multichain news. It is a difficult situation for everyone impacted, on a brighter note we have found an alternative to swap Multichain Assets using our https://fwallet.network inbuilt Dex Aggregator. USDC holders can now swap their funds to $FTM at $1 price using the Dex Aggregator,” the tweet read.

Since the beginning of July, the total value locked (TVL) in the Fantom network had been on a sharp dive owing to the Multichain saga. The TVL had fallen by 67% on July 16 in July only. This makes it one of the biggest hits in the network’s operational history.

Keep watching FinTech Express for more updates on this and other fintech-related developments.

Celsius has sold another huge batch of crypto assets despite the US lodging an investigation against it.

The sell-off comes days after CEO Alex Mashinsky was arrested and is being charged with fraud in the US.

Bankrupt crypto lender Celsius Network has sold significant crypto assets despite being investigated by the US. The sell-off comes days after the US arrested the lender’s CEO, Alex Mashinsky.

Celsius Network converting its crypto holdings

According to data from the Onchain platform, LookonChain, Celsius is selling its altcoin holdings. The on-chain data platform indicated that Celsius sold off assets as follows: 1.27M LINK ($8.5M) 2.83M SNX ($7.84M) 12,597 BNB ($3M) 4.45M 1INCH ($2.26M) 8.53M ZRX ($1.9 M) 439K FTT ($713K) into FalconX 186,149 BONE ($235K) into OKX.

The assets transferred to FalconX were then deposited into Binance for sell-off. Lookonchain was alarmed that Celsius began swapping its altcoins for Bitcoin and Ethereum on July 6, taking its total public altcoin holdings to $164.5 million held on the EVM Chain.

Celsius Network has been selling off its crypto holdings for quite some time now since it went ‘bankrut.’ The current sell-off comes after court approvalon June 30 to convert its altcoin holdings into Bitcoin and Ethereum before redistributing the same to its creditors.

The development comes days after the US arrested its CEO Alex Mashinsky last Thursday on allegations of fraud. Alex Mashinsky is expected to fight charges against different regulators and the DoJ, making his situation the latest high-profile crypto lawsuit this year.

Keep watching Fintech Express for more updates on this and other fintech-related developments.

Cameron Winklevoss has called out the US SEC for its bad crypto regulations following the Ripple case partial loss.

The Gemini boss has expressed that some SEC’s practices, such as allowing companies like Coinbase to go public only to charge them later, are ludicrous.

Gemini boss Cameron Winklevoss has expressed dissatisfaction with the US SEC’s unrealistic crypto regulation approach. He pointed out on Coinbase story where the US SEC allowed it to go live only to charge them later, calling it “ludicrous.”

SEC allowing a company to go public and then charging it is ludicrous- Cameron Winklevoss

Coinbase is one of the many crypto organizations that are ‘victims’ of the US SEC’s regulatory sword. The crypto exchange has featured in a high-profile lawsuit where the US SEC alleges that it is trading crypto securities in the country without its permit.

Coinbase has, however, challenged the allegation that it cleared with the regulator long before going live. However, the US SEC still feels that more needs to be done. In a Thursday court proceeding, SEC lawyers claimed that simply because it allows a company to go public doesn’t mean it has its blessings.

“Simply because the US SEC allows a company to go public, it does not mean that it is blessing the company’s business,” said SEC’s Peter Mancuso.

This statement has come through as a trap for companies, as the US SEC should only have allowed a company to go live in the first place if it was satisfied with the business it had outlined in the initial filing.

Judge Faila replied to Mancuso, saying she was skeptical about the whole saga and would have thought that the form S-1 (a registration file) would have involved due diligence. She added:

“They (referring to SEC officials) could have said, ‘Hey, you have filed as a securities exchange.’ That was within their power was it not?”

Cameron Winklevoss has come out against the US SEC for doing this to Gemini, saying it’s ludicrous. Keep watching Fintech Express for more updates on Coinbase vs. SEC and other Fintech-related developments.