Key Points

- Bankrupt crypto lender BlockFi is working on blocking FTX and 3AC from retrieving millions in loan payback.

- FTX and 3AC had lent money to BlockFi but underwent bankruptcy in 2022, necessitating the payback of loans given to the crypto lender.

In an August 21 filing in a New Jersey Bankruptcy Court, BlockFi claimed that its creditors should not be pushed as FTX’s creditors were harmed by the exchange’s misappropriation of $5 billion that BlockFi had lent it. It also added that bankrupt crypto hedge fund 3AC committed fraud with the money lent and thus should not be entitled to a potential repayment.

BlockFi tries to block 3AC and FTX from retrieving millions in payback

BlockFi, FTX, and 3AC were some of the largest crypto fraud and bankruptcy cases ever seen in the industry’s history. They “coincidentally” happened in the same year and conspicuously had ties to each other.

As such, there have been multiple tussles between these organizations as they try to repay their dues to creditors and refund users’ money simultaneously. BlockFi, a bankrupt crypto lender, has been pushing for long that FTX and 3AC not get paid from its liquidations as they may have misappropriated the money it lent.

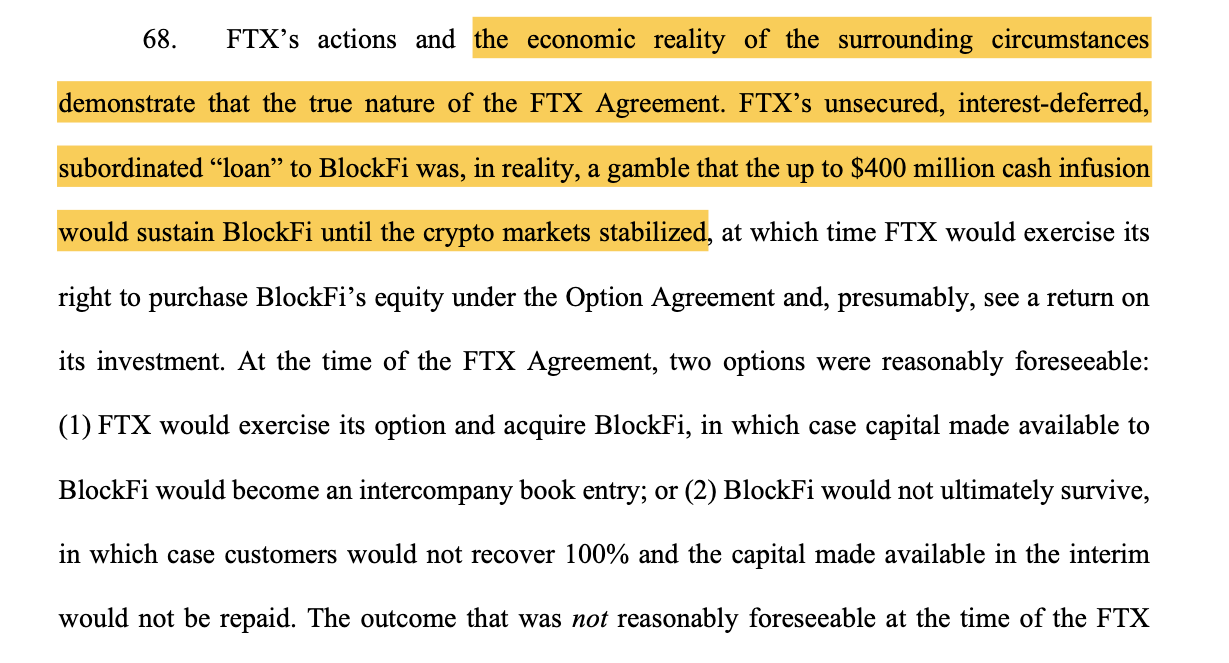

Estimates show that BlockFi owes around $ 10 billion to over 100K creditors and $! Billion to three of its largest ones. In the mix of freditors comes 3AC and FTX. It owes 3AC about $220 million and FTX around $400 million. FTX and 3AC have been pushing to get these hundreds of millions back as they would make it much easier to repay their creditors.

However, a recent Court filing shows that BlockFi feels the two creditors are the real victims in the case. An excerpt from the filing reads:

“FTX seeks to recover on over $5 billion of claims filed against the BlockFi estates at the direct expense of the ultimate victims of FTX’s fraud: BlockFi’s clients and other legitimate creditors.”

“To prevent further injustice to the creditors of BlockFi’s estates, the Court should disallow the FTX claims under the doctrine of unclean hands,” BlockFi added.

BlockFi further indicates that the $400 million FTX gave wasn’t a standard loan as it was under an agreement to have a five-year term that would not activate until the firm supposedly matures. As such, BlockFi feels that it should be treated as a “gamble” for which it should not be liable.

Despite the ongoing skirmishes, creditors recently settled with BlockFi in July to proceed with the set repayment plan. However, it is still yet to be seen if it will work out as 3AC and FTX’s $1 billion loans would significantly affect its creditors’ payout. Keep watching Fintech Express for updates on this and other fintech-related developments.